What Exactly Is Foreclosure?

Most people see foreclosure as you can’t afford your mortgage or your bank is taking the house back, but that’s oversimplifying things a bit. Foreclosure is the legal right that a mortgage holder or any other lender that provided you with the means to buy your home has.

If the mortgage or lien is in default, they have the means to start the legal process of foreclosure to gain ownership of the property. There can be a variance from state to state, but generally, there are two main types of foreclosure most people go through:

- The first type of foreclosure is foreclosure by judicial sale, which is required in most states. Basically, the mortgaged property is sold under court supervision, with proceeds satisfying the mortgage, followed by anyone else who holds a lien on the home. This qualifies as legal action.

- The second type of foreclosure is foreclosure by power of sale. Here, the mortgage holder sells the property without court supervision. Generally, it’s going to be faster to do it this way than doing it through the courts, and other states allow for this. There are other issues with this route, which we will discuss later on.

On top of the obvious issue of losing your home, foreclosure can also have a long-lasting effect on your credit score. This can make it more difficult down the line for you to secure a future place to live, or only having riskier high-interest loans and funding as options.

What Scenarios Lead To Foreclosure?

In the financial world, things rarely strike without warning. Ideally, you budgeted to keep up with your mortgage payments every month before you even brought the house, but there may be things that impact your ability to keep with the allotment you originally mentioned.

In other cases, it may be the nature of the mortgage you took that causes financial hardship. Here are some of the common issues that tend to cause foreclosure.

Adjustable-Rate Mortgages

To be clear, for some people, this may make the most sense for funding a house purchase. Where issues start is not knowing what the pros and cons of these mortgages entail. These tend to start low in terms of interest rates, but reset down the line with a much higher rate.

If you’re not prepared, this may make the difference between a mortgage you can afford each month and one you can’t. Many people end up in foreclosure because they don’t understand or didn’t read the terms of their mortgage.

Loss of Earning Power

Unlike the previous issue, this can put you on the path to unemployment through no fault of your own. While there are programs out there to help people who have lost their jobs and the means to help pay for their homes, nothing is guaranteed.

In addition, sometimes, the process of applying to these programs and getting aid may take too long, especially if your lender is already threatening to take the home. Since, in many cases, losing your job is something out of your control, the best option you have is to try and put together an emergency fund with a few months’ worth of mortgage payments. At least this way, should the worst happen, you have some time to find employment before your home is at risk.

Household Changes

It’s a bit difficult to try and sum up this category, but to put it as simply as possible, there are many different things that can happen to a household that would affect their finances to the point where an affordable mortgage becomes too much.

Examples of these can include medical emergencies that suddenly drain funds and savings out of the blue. If the primary breadwinner in a family was to pass away, there’s a permanent loss of earning power in that household.

In addition, situations like divorce may lead to foreclosure, directly or indirectly. Directly, the legal expenses of a prolonged case may end up causing financial hardship. Indirectly, a couple may have only been able to pay the mortgage on a house together, and if one is left with the property, they may not be able to manage.

Managing Multiple Properties

Compared to other situations, it’s rare that a person finds themselves suddenly on the hook for multiple mortgages. When this does happen, you may have your finances spread too thin to keep up.

For example, perhaps you needed to relocate before actually selling your home for a job or other reasons. Another situation may occur when you inherit a property upon the passing of a relative. When this happens, you may live too far away from the property to use it or you may not want it in general.

How Does the Foreclosure Process Work?

Whether it’s one of the above reasons or something else, it’s important to understand that foreclosure doesn’t mean you instantly lose your home the first time your mortgage payment is late. The first thing that will happen when you miss a payment is that you will get some sort of notification from your lender, either through the mail, over the phone, or both. These explain how much money you owe and a way that you can go about submitting your late payment. This puts you into the pre-foreclosure stage.

If this is a simple case where you just forgot to send the money that month, chances are that you’re not going to be in much trouble. The bulk of mortgage payments are due the first of the month, with a grace period until the 15th. Should you miss that and pay, you’ll probably get the letter as mentioned and a late payment fee for your trouble.

After two payments are missed, you get a more serious letter of demand at this point. The lender will most likely still be willing to work with you, but you want to be all paid up within 30 days of receiving it.

It’s when you hit the 90-day mark with no payments that most lenders start to get really serious, sending a notice of default. If you don’t meet provisions of the letter of default in the appropriate time, your house will be foreclosed. The lender will generally demand acceleration of the loan, which means you now have to pay the entirety of the debt rather than just your missed monthly payments.

Assuming that you’re going through a judicial foreclosure, the lender will file a lawsuit with the county to seize and sell the home to pay off debts. Legally, you have the right to try and fight this in court, but even if you don’t want a prolonged legal battle, it’s a good idea to respond to the lawsuit. Failing to do so forfeits your right to fight the foreclosure.

Let’s say that your lender ends up getting a foreclosure judgment. At this point, your lender also has the ability to issue a Notice of Sale, likely the part of foreclosure that you should be most concerned about.

Also known as the notice of trustee, the document tells the borrower that the lender is going to sell the property, and will give an auction date as well. This lender will likely publish this notice in local newspapers to let people know the property is for sale.

Following the sale itself, the highest bidder will get a certificate of title or deed of trust, and the sale proceeds will be distributed to the lender. You can request for time to move out of the property, but your lender is not beholden to the request by any means, and you may have to leave right away.

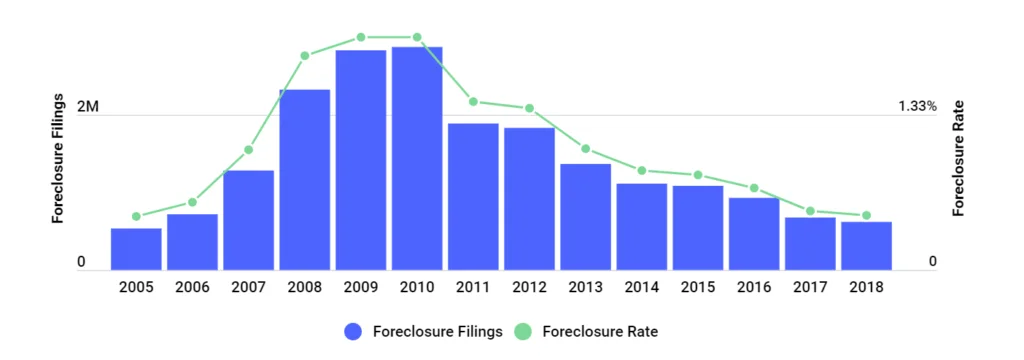

The good news? Mortgage delinquencies have fallen from their heights during the economic bust a few years back.

The bad news? Many people are still behind on their mortgages. In fact, five percent of U.S. mortgage payments are delinquent by 30 days or more.

Homeowners behind on their mortgage find themselves between a rock and a hard place unable to make payments and staring at unsavory, credit score-crushing options.

But if you’re one of them, you DO have options. We present the most common ones below, as well as their upsides and unfortunate downsides. Think of the following as an open house.

Only instead of walking through a prospective home to get a closer look, you’re walking through and getting a closer look at the foreclosure options available to you if you can no longer afford your mortgage, including selling your home fast.

Learn more about these mortgage options:

1. Reverse Mortgage

What Is a Reverse Mortgage?

The Consumer Financial Protection Bureau (CFPB) puts it best:

A reverse mortgage is a type of loan that allows older homeowners to borrow against the equity in their homes. It is called a reverse mortgage because instead of making payments to the lender, you receive money from the lender.

Pros

Reverse mortgages can help you access the equity in your home to handle day-to-day expenses and emergencies, establish an equity line of credit, and more.

Cons

Do you want to leave your home to your children? Is the loan only in your name and not your spouse’s? Could you be moving anytime in the near future? Do you anticipate any problem at all making payments on property taxes, homeowners insurance, and/or home maintenance?

If you answered yes to even one of those questions, a reverse mortgage can complicate your finances at best and at worst, leave you or your heirs without a house.

2. Loan Modification

What Is Loan Modification?

Law website Nolo.com describes loan modifications for mortgages as a permanent restructuring of the mortgage where one or more of the terms of a borrower’s loan are changed to provide a more affordable payment. Modified terms may include interest rate and the length of the loan.

Pros

A loan modification can lower your mortgage rate, decrease your loan term, and bundle closing costs into the new loan.

Cons

There are a lot of loan modification scams. A whole lot. Separating the good guys from the bad guys is almost a cottage industry in and of itself. MakingHomeAffordable.gov has some information that helps, as does the Federal Trade Commission. A loan modification can be very beneficial, but you need to advance carefully to avoid falling prey to a mortgage relief scam.

3. Refinancing

What Is Refinancing?

Refinancing your mortgage means you are replacing the old mortgage with a new one that includes terms more favorable to you; a lower interest rate, for example. This is how refinancing a loan is different than modifying a loan: modifying a loan makes some adjustments to the loan but keeps the same loan in place.

Pros

Refinancing a loan can improve the terms for you, such as decreasing your interest rate.

Cons

Getting the most out of a mortgage refinancing scenario requires the stars to align just so: you’re not planning on moving soon, your credit is good, you won’t have a problem paying closing costs, you’re not interested in tapping into your home’s equity and so on.

For some people, that’s enough stargazing to require a call to both your mortgage lender and Neil deGrasse Tyson.

4. Short Sale

What Is a Short Sale?

From the CFPB: A short sale, which is a type of loss mitigation, is a sale of your home for less than what you owe on your mortgage.

Pros

If you can swing a short sale, it’s possible that you’ll be able to pay off your mortgage even if the sale brings in less money than the balance remaining on the loan. Plus, any time you can avoid foreclosure, things aren’t all that bad.

Cons

We’re now at the stage of our mortgage affordability options open house where your credit score will take a hit. Possibly a big one. A short sale can take your credit score down by as many as 125 points.

Why do you need to worry about your credit score? Because your credit score helps creditors determine whether to give you credit, decide the terms you are offered or the rate you will pay for the loan. A good score makes it easier to get a loan, rent an apartment, and qualify for lower insurance rates.

5. Deed in Lieu of Foreclosure

What Is Deed in Lieu of Foreclosure?

In a deed-in-lieu of foreclosure agreement, your lender assumes ownership of your home rather than have it enter the foreclosure process. It’s often considered alongside a short sale and only marginally better than a full-on foreclosure.

Pros

The primary way a deed in lieu of foreclosure is helpful? It isn’t a foreclosure. There aren’t many helpful turns at this stage in our open house tour.

Cons

Some experts believe that your credit score suffers from a deed in lieu of foreclosure as much as it would an actual foreclosure. Factor in any damage your credit score received from missed mortgage payments, and you have a scenario that will haunt your credit score for a long time.

And if you plan on buying another home, make sure those plans are no sooner than two years off, and maybe as many as four years. That’s how long Fannie Mae and Freddie Mac will wait before purchasing mortgages under a deed in lieu of foreclosure circumstances.

Lenders are also hesitant to agree to deed-in-lieu of foreclosures. Why? They worry the homeowner could sue at a later date and claim they didn’t understand what they were doing; they’re on the hook for any second or third mortgages the homeowner may have; and finally, they want to be certain the financial distress is real.

6. Foreclosure

What Is Foreclosure?

USA.gov defines a foreclosure as a situation in which a homeowner is unable to make mortgage payments as required, which allows the lender to seize the property, evict the homeowner, and sell the home.

Pros

A foreclosure helps in that it alleviates the stress and pressure the homeowner feels over missed mortgage payments and an uncertain future.

Cons

You can no longer live in the place you call home. Foreclosures can damage your credit score to the tune of 250-280 points and may stick around on your credit report for as many as seven years. Foreclosure is so damaging to your credit that it can make your whole life more difficult, from applying for a credit card to renting an apartment.

You’ll face years of expensive and limited credit opportunities. You may even face limited job opportunities since some employers look at credit scores when evaluating potential applicants. You’ll also need to wait three to seven years in order to buy a home again.

Sadly, the consequences of foreclosure don’t stop there. The list of long-lasting and debilitating downsides just keeps growing. Consequences include:

- An embarrassing and public eviction from your home

- Uncertainty and stress of not knowing exactly when you’ll leave your home or where you’ll go

- Owing a deficiency balance after the foreclosure sale

- Losing any relocation assistance or leasing opportunities that may be available if you avoid foreclosure

- Forfeiting the ability to get a Fannie Mae mortgage to buy another home for at least seven years

And the final nail in the coffin of foreclosure? The stress and angst over foreclosures have encouraged many scammers to take advantage of unsuspecting homeowners struggling to pay their bills. It’s best to avoid foreclosure at all costs.

7. Bankruptcy

What Is Bankruptcy?

Bankruptcy, specifically chapter 13 bankruptcy, allows people with regular income to repay all or part of their debts over anything from three to five years. An important feature is that it can help homeowners avoid foreclosure.

Pros

Filing bankruptcy provides some breathing space to people faced with severe financial hardships, a chance for them to receive the support necessary to address their income problems.

Cons

This option does the most significant amount of damage to your credit score, wiping out anywhere from 130 to 240 points. A bankruptcy can stay on your credit report for as long as a decade. As far as personal finances are concerned, bankruptcy is a weapon of mass destruction best avoided if at all possible.

8. Sell Home Fast for Cash

What Is Selling Your House Fast?

Refinancing, foreclosing, filing for bankruptcy: all are options the struggling homeowner can leverage when behind on a mortgage. But selling your house to a new owner can be the fastest and most fiscally viable path, one that won’t linger on a credit report and leave you indebted to a years-long recovery process.

In fact, selling a home fast for cash is an option some homeowners aren’t even aware of.

Pros

An outright sale has the potential to alleviate financial pressure and emotional stress, generate quick funds for the next chapter in your life, and get it all done within a relatively brief period of time.

Choosing HomeGo to usher you through the process also means you don’t have to waste time or money making repairs, deal with the aggravation of one unexpected showing after another, concern yourself with the uncertainty of lenders, or pay commissions, closing costs, or service fees. Of all the paths available to a homeowner struggling with their mortgage, this one carries a lot of pros for those you can’t afford their mortgage.

Cons

Even though the property has likely gone from a dream come true to a heavy burden, it’s still a place that seemed very special at one point in your life. Letting go is hard. It’s only natural to feel this way.

Find Your Solution with HomeGo

Tackling all of the problems that arise from struggling to pay a mortgage exacts a higher toll mentally and financially than many people realize. That’s one of the reasons every expert suggests dealing with the issue as soon as possible rather than postponing it.

But if you’re at a point where looking at foreclosure and bankruptcy, you owe it to yourself to invest 10 minutes with HomeGo on a brief tour of the home to see what we could offer you for it.

A fast home sale may be your best route to a better tomorrow, especially if you’re so far behind on the mortgage that you simply can’t afford to keep up. It could even help save your credit. For homeowners seeking speed, convenience, simplicity, and a stress-free home sale, get an offer here. We’re here for you no matter your situation.