The Federal Housing Administration (FHA) insures mortgage loans made by FHA-approved lenders to help people become homeowners. FHA loans benefit first-time home buyers and those with lower credit scores or limited income. Since the federal government backs FHA loans and covers losses if a borrower can’t pay their loan in full, FHA loans have lower financial requirements and require lower down payments than conventional loans.

What Is an FHA Loan?

An FHA loan is a mortgage the FHA insures. The FHA has been insuring mortgages since 1934 and is one of the world’s largest mortgage insurers. It does not fund loans but instead provides insurance to cover loans made by FHA-approved lenders. The insurance covers losses if borrowers are not able to fully pay back a loan.

The federal government backs bank and credit union FHA loans, which means the FHA can guarantee lenders that losses will be covered if a homeowner doesn’t pay back a loan in the full amount. FHA loans are available to a variety of borrowers, but they are especially beneficial for buyers who will live in the house full time and first-time home buyers.

What Does an FHA Loan Do?

FHA loans reduce risks for banks and lenders, allowing them to offer lower down payments for borrowers with lower credit scores or income. The FHA insures loans for individuals with lower income and credit, but there is no income limit to receive FHA loans. Anyone who meets the minimum qualifying standards can receive an FHA loan.

The Department of Housing and Urban Development (HUD) provides a lender search tool to help borrowers check if their lender is FHA-approved. From there, a lender can help them determine if they are eligible for an FHA loan.

What Are the Requirements for an FHA Loan?

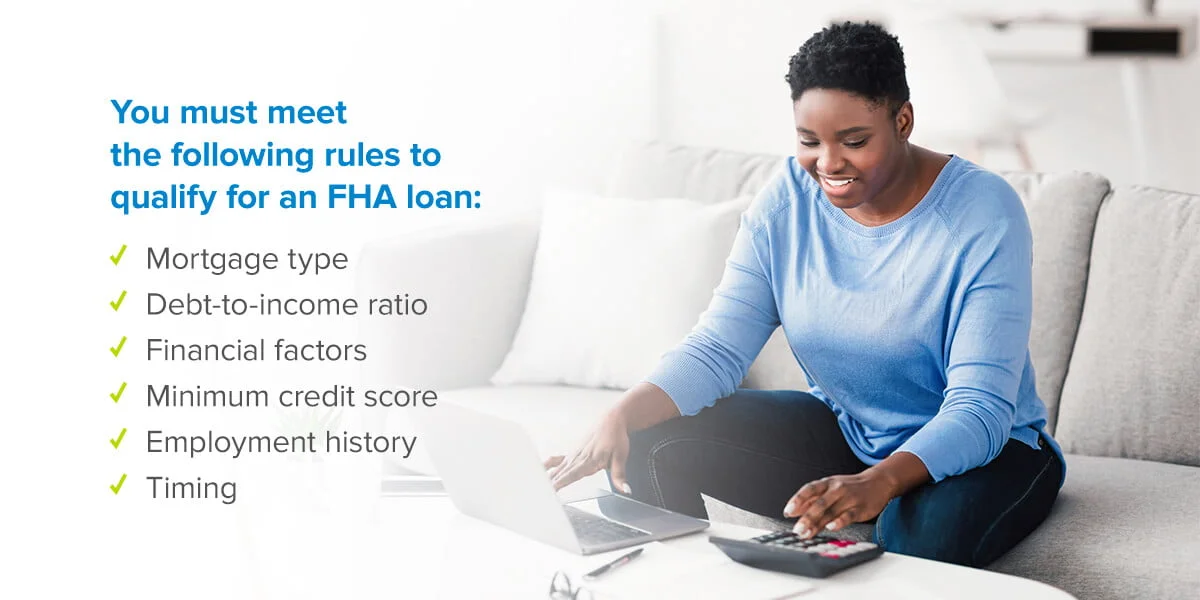

FHA-approved lenders must follow certain regulations to grant an FHA loan. It’s important to know who is qualified for an FHA loan before deciding if it’s right for you. Your available down payment amount and your credit scores will affect the lending process. Additionally, you must meet the following rules to qualify for an FHA loan:

- Mortgage type: The home you plan to buy, renovate or refinance must have between one and four units. Additionally, you must plan to live in the house as your primary residence.

- Debt-to-income ratio: Your total front-end debt ratio, which includes your monthly mortgage payments, should be 31% or less of your gross monthly income. Your total monthly back-end debt ratio, which includes your monthly debt payments and mortgage payments, should typically be equal to or less than 43% of your gross income.

- Financial factors: Your lender must verify your income, credit and your desired property’s value. You can provide income verification through pay stubs, bank statements and federal tax returns.

- Minimum credit score: An FHA loan requires a minimum FICO credit score of 500 to 579 to qualify for a loan with a 10% down payment. You need a score of 580 or higher to qualify for a loan with a 3.5% down payment.

- Employment history: You need proof of employment history for at least the previous two years. You’ll need to explain employment gaps that span a month or more and have proof of enrollment in schooling or the military if you haven’t worked in the past two years.

- Timing: If you file bankruptcy, you should wait at least two years to apply for an FHA loan. Additionally, you should wait three years after a foreclosure to apply.

It’s also important to know what homes qualify for FHA loans. Home buyers can use FHA loans to refinance or buy single-family homes, two to four-unit multifamily homes, condominiums and some manufactured homes. Some FHA loans cover new home construction or existing home renovations.

FHA vs. Conventional Loans

To help you further understand what an FHA loan is, consider how it differs from a conventional loan:

Government Backing

Conventional loans lack government insurance, whereas the government backs FHA loans. The government will cover losses on FHA loans that borrowers cannot fully pay, but the government will not cover losses on conventional loans.

Borrower Requirements

To qualify for a conventional loan, borrowers must have a solid income, higher credit score and at least a 3%-20% down payment for certain loan programs.

The credit score needed for an FHA loan is much lower than conventional loans, which typically require a credit score of 620 or higher. Conventional loans also typically require a higher down payment than FHA loans.

Loan Terms

Conventional loans are usually for 8- to 30-year terms, while FHA loans are usually for 15- to 30-year terms. Conventional and FHA loans are available at fixed or adjustable rates.

Insurance

Conventional loans require private mortgage insurance if you put less than 20% down. FHA loans will require insurance no matter how much or how little you put down.

Since individuals with lower credit scores are considered riskier to provide loans to, those individuals must protect lenders by paying mortgage insurance. FHA loans require the following mortgage insurance premiums:

- Annual mortgage insurance premium: You will need to pay an annual mortgage insurance premium of 0.45% to 1.05%, depending on the loan’s amount, term and initial loan-to-value ratio (LTV). Your annual mortgage insurance premium will be divided by 12, so you can pay it monthly.

- Upfront mortgage insurance premium: When you receive an FHA loan, you will need to pay 1.75% of your loan’s amount. You can choose to roll this premium into your financed loan amount if you wish.

Even though you will pay higher mortgage insurance premiums and more interest over time, an FHA loan is ideal if you have a limited income or lower credit scores.

Sell Your Home With HomeGo

An FHA loan can help you move into a home even if you have limited income or a lower credit score. FHA loans require lower down payments than conventional loans, allowing you to move quicker than you would if you needed to save money for a higher down payment. HomeGo can also help you speed up the moving process. With HomeGo, you don’t have to wait for potential buyers to see your house and make offers because we will purchase your house for you.

HomeGo will purchase your current home as-is, no matter what condition it’s in. Our agents will visit your home, complete an assessment and make a cash offer on the spot. Avoid hidden costs and sell your home quickly and easily. With HomeGo, you can decide when you are ready to move out, and you can close in as little as seven days. Contact HomeGo to learn more about selling your home.